Capital Contributions

How to record capital contributions in Bkper, including the difference between debt and non-debt contribution agreements.

A capital contribution is an act of giving money or assets to a company or organization.

There are two main types of contribution agreements. The first requires the business to take on a debt — essentially a loan payable. The second lacks the characteristics of debt: there is no execution date, no interest, and the capital does not necessarily have to be paid back.

Capital contribution agreements are usually made with investors, but they can also come from someone interested in partnering with your company.

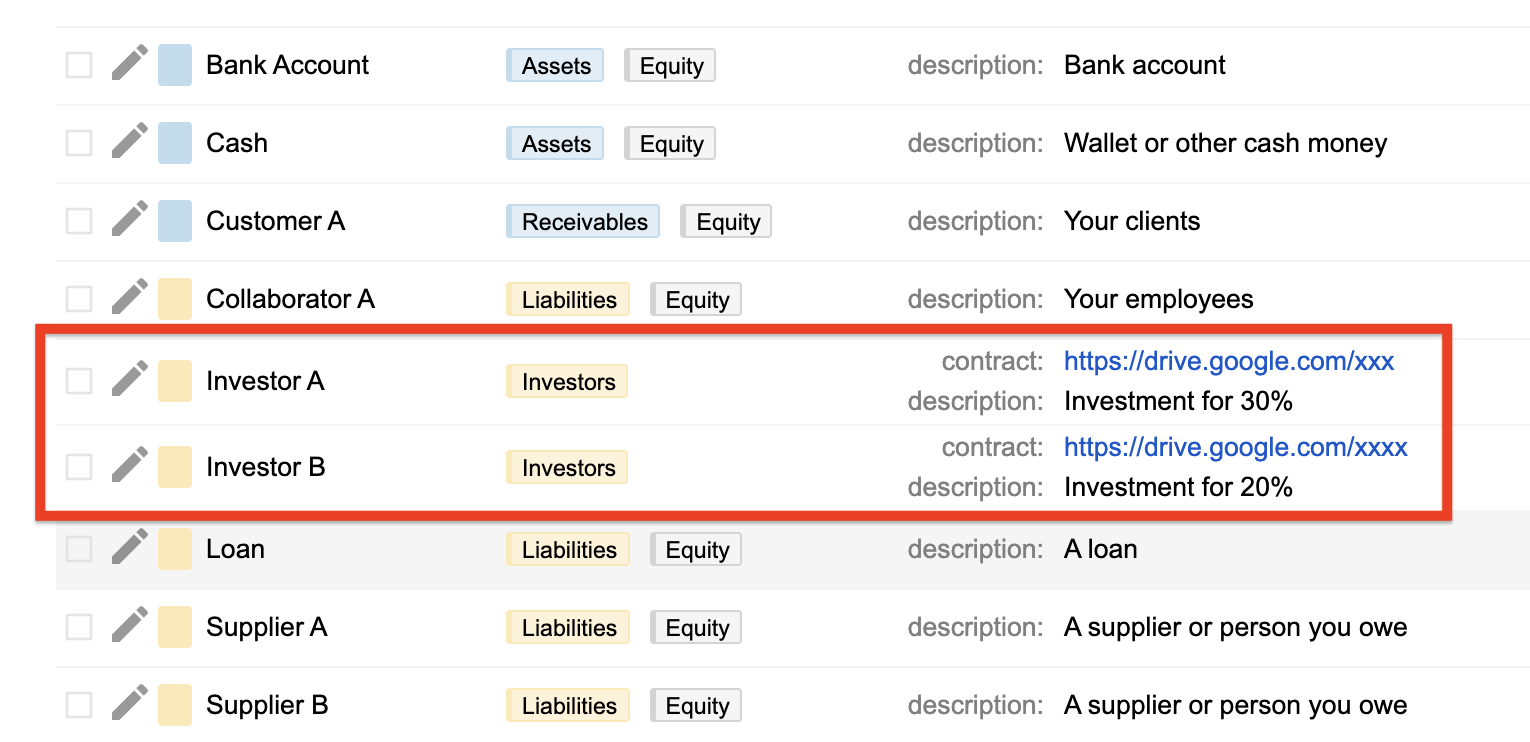

Both types of contributions are represented by the Liability Account type, which holds a permanent “From Account” balance.

The key difference in how you record them in Bkper is that non-debt agreements are included in the Equity Group, while debt agreements are not. Non-debt contributions increase the Equity of the business and should not appear as an account payable on the balance sheet. Debt-like contributions remain liabilities and are better grouped with other obligations, such as loans payable.